Extracted from BT online

June 7, 2008

PREFERENCE shares have been hitting the headlines lately. First there was DBS Bank's $1.5 billion issue which drew much flak for shutting out retail investors. OCBC Bank, on the other hand, decided to offer its $1 billion preference shares to both institutional and retail investors.

Both DBS's and OCBC's preference shares are attracting a lot of demand because of their high dividend yields. In DBS Bank's case, the issue pays 5.75 per cent in the first 10 years, before becoming floating-rate notes paying 3.415 percentage points above the three-month Singapore dollar swap rate. OCBC pays a fixed dividend of 5.1 per cent.

Two readers have written to me, hoping that this column could help explain some of the technicalities of preference shares. And coincidentally, both of them brought up City Developments' preference shares. So we'll look at preference shares this week.

First, some basic knowledge. Preference or preferred shares, as the name suggests, have priority over common or ordinary shares when it comes to dividends and entitlement to the proceeds of sale or liquidation. In exchange for this privileged position, preferred shareholders usually give up their right to participate fully in the success of the company. In other words, if the company stumbles onto a new technology that will earn it a lot of money in the years to come, common shareholders are likely to see their share price rise significantly in anticipation of the bigger share in the profits that they are entitled to.

Preference shareholders, on the other hand, will only be entitled to the fixed dividends. Instead, the price of the preference shares will react to the general movement of the interest rate in the market. If the market interest rate goes up, the price of the preference shares will fall, and vice versa.

Redeemable by holders?

Dividend payments for the preference shares can be cumulative or non-cumulative. For cumulative preference shares, if, say, the company does not have the cash to pay out the dividends this year, it will have to pay out this year's dividends, as well as next year's, the following year. Dividend arrears must be paid before any dividend can be paid to common shareholders.

Preferred shares are almost always callable by the issuer, which means the company can decide to buy back the preference shares from the investors after a certain date. In DBS Bank's case, it can redeem the preference shares after June 2018.

Some preference shares, however, are redeemable by the preferred shareholders, often over a period of years with a guaranteed future value for the shares. In analysing companies with such preference shares, one should treat the preference shares as debt. They should be included as debt in solvency ratios, and the dividend payments should be treated as interest. Also, such redeemable preferred shares should be excluded from shareholders' equity.

There is one point which investors have to note, though. Companies cannot be forced to pay the dividends or redeem the preferred shares. Unlike creditors, preferred shareholders do not have the power to force the company into bankruptcy for non-compliance with the terms of the agreement.

Another form of preferred shares can be converted into common shares. CityDev's preference shares are one such instrument.

Now, let's look at CityDev's preference shares more closely.

CityDev's preference shares - issued in 2004 - are non-cumulative and do not have fixed dividend payout. Its board of directors will decide on the rate every year, but the payout will not exceed 3.9 per cent (net) per year over its issue price of $1. The board is under no obligation to make any dividend payment.

The preference shares, however, are convertible to CityDev's ordinary shares any time after the second anniversary of their issue. But only the company can decide if and when they want to do the conversion. The holders have no say in the matter.

One thousand preference shares can be converted to 136 ordinary CityDev shares. In other words, it would take 7.35 preference shares to convert to one CityDev share.

In the event that CityDev exercises its right of conversion, it will pay the holders of preference shares a one-off additional preference cash dividend of 64 cents per share.

As of yesterday, the preference shares were selling for $1.79 and CityDev's shares were last traded at $11.18. The two readers pointed out to me that the preference shares are trading at a huge discount to the ordinary shares.

Let's work through the numbers. It takes 7.35 preference shares to get one ordinary share. And when they are converted, each preference share will receive 64 cents.

So one preference share is entitled to 1/7.35 ordinary shares. Based on the last transacted price of CityDev yesterday, one preference share can be exchanged for 1/7.35 of CityDev's ordinary share of $11.18. That works out to $1.52.

But when there is a conversion, the preference shareholders will receive cash of 64 cents per preference share. So theoretically, based on yesterday's price, the preference shares should be trading at $1.52+$0.64, which is $2.16.

Given that the preference shares are selling at $1.79, there appears to be a 'discount'.

But wait. Only CityDev can decide if and when it wants to convert the shares. And it can decide never to do so because the preference shares are a perpetual instrument.

If this is the case, then investors are holding on to something that pays no more than 3.9 cents a year. That's a yield of zero to a maximum of 2.2 per cent (over $1.79). The exit for investors, if CityDev does not convert the shares, will be to sell the shares in the market. The problem with this is, the instrument is very illiquid. No trade was done yesterday. There was a wide spread in the bid and offer prices. A buyer was willing to buy at $1.46 and a seller was willing to sell at $1.79.

Hence the 'discount' is to take into account the numerous negative attributes of the instrument.

In comparison, there is certainty in the dividend payout of the DBS Bank's and OCBC Bank's preference shares, and the yields are attractive, given the current interest rate environment. This explains the relative attractiveness of the banks' preference shares vis-a-vis CityDev's.

A 5 to 6 per cent yield is undeniably attractive. But this sort of yields may not be that difficult to find among the stocks trading on the Singapore Exchange given the current depressed stock prices. If some of the these companies keep up the same amount of dividends they paid in the last financial year, yields of up to 10 per cent can be pocketed.

Good dividends

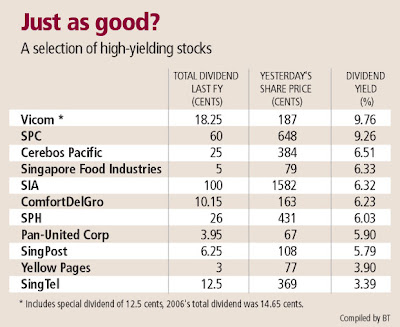

I've compiled some of the stocks which paid out relatively generous dividends last year. (see table)

Vehicle inspection and testing service provider Vicom last year paid out 18.25 cents of dividends. Compared with a traded price of $1.87, the yield worked out to be 9.8 per cent. Of course, included in last year's dividend was a special payout of 12.5 cents. But, there was one special dividend too in 2006. That year, the total payout amounted to 14.65 cents.

Singapore Petroleum Company paid out a dividend of 60 cents last year. That's a yield of 9.26 per cent based on a traded price of $6.48.

Cerebos Pacific, Singapore Food Industries, Singapore Airlines, ComfortDelGro and Singapore Press Holdings, if they keep up their last year's payout, will all be yielding above 6 per cent.

The question, of course, is whether companies paying good dividends can maintain their dividend policy. For a few of the companies mentioned, they enjoy a strong franchise and are generating cash by the oodles. And for one or two, the business prospects actually look good going forward. So there are still attractive investments out there that do not carry too much risks.

The writer is a CFA charterholder. She can be reached at hooiling@sph.com.sg

Sgbluechip says: Starhub is also a defensive dividend stock. At current price of $2.87, dividend yield is 6.27%. Management have indicated that it will be distributing a minimum of $0.18 per share dividend for FY 08.

I do agree that valuations of dividend stocks are depressed due to poor market sentiments. However, transportation theme stocks will still face downward pressure due to uptrending crude oil prices.